You’re scrolling through Instagram again. Another friend is sipping an Aperol spritz in Positano—and you’re wondering: what’s the best way to save for a big trip on a tight income? Here’s the truth: you absolutely can save for a big trip on a tight income. No lottery win required. No moving back in with your parents (unless you want to). What you need is a system that works with Australian reality – rising rents, casual work hours, and the occasional smashed avo without shame.

- Why Saving Feels Impossible (And Why That’s Not Your Fault)

- Your Step-by-Step System to Save for a Big Trip on a Tight Income (Without Burning Out)

- Step 1 – Set a ridiculously specific trip cost

- Step 2 – Reverse-engineer your weekly target

- Step 3 – Automate before you see the money

- Step 4 – Attack one spending leak per fortnight

- 5 Micro-Saving Apps That Work in Australia (Set & Forget)

- The ‘Invisible Money’ Strategy – Rewards, Cashback & Points (Without Extra Spending)

- Realistic Side Hustles for Time-Poor Aussies (No Uber Eats Marathons)

- Airtasker for micro-gigs

- Market research & user testing

- Selling digital clutter

- The ‘one side hustle shift = one travel day’ rule

- How Much Do You Really Need to Save for Your Dream Trip? (Real Australian Examples)

- The 3-step formula (featured snippet ready)

- Example 1 – Bali on a budget (10 days)

- Example 2 – Europe backpacking (4 weeks)

- Example 3 – Japan moderate budget (2 weeks)

- How Sarah from Brisbane saved $3,000 in 6 months on a $55k salary?

- The 3 Most Common Ways Australians Sabotage Their Travel Savings (And How to Fix Them)

- Realistic Timelines Based on Your Income (Be Kind to Yourself)

- How to Stay Motivated When Saving Feels Slow (The Visual Trick That Works)

- FAQs

- Is it realistic to save for a big trip on minimum wage in Australia?

- What’s the best bank account to save for travel in Australia?

- How do I save for a trip when I still have HECS debt?

- Can I use my superannuation to fund a big trip?

- What’s the fastest way to save $3,000 on a tight income?

- You Don’t Need More Money. You Need a Different System.

Let’s build that system together.

Why Saving Feels Impossible (And Why That’s Not Your Fault)

Let’s get real for a moment. You’ve probably tried the whole “just cut back on coffee” advice, and surprise – it didn’t fix everything. That’s because you’re dealing with structural pressures, not just individual spending habits.

Right now, Aussie renters face a triple squeeze:

- Housing: ~30% of income goes to rent in Sydney/Melbourne

- HECS/HELP: Repayments start at $54,435 income threshold

- Essentials: The ABS reports that Aussie households are spending nearly 8% more on essentials than two years ago – and you can feel it at the checkout

If you’re on a casual or part-time income – common for students and young professionals – your pay can vary wildly from week to week. That makes traditional “save 20% of your income” advice feel like a joke.

Here’s the truth that most finance blogs ignore: tiny sacrifices don’t create meaningful change when your baseline is already tight. Saving $5 a day on coffee adds up to $150 a month, yes. But if you’re already only buying two coffees a week, there’s nothing left to cut.

What actually works is building small, systemic changes into your money flow – before you even see it. That’s what we’re about to do.

Your Step-by-Step System to Save for a Big Trip on a Tight Income (Without Burning Out)

Forget deprivation diets. This is a four-step system designed for actual humans with actual social lives.

Step 1 – Set a ridiculously specific trip cost

Vague goals like “save for Europe” don’t work. Your brain needs a number. Here’s how to find yours:

- Flights: Open Skyscanner or set up price alerts on Google Flights to track fare drops for your dream destination—many Australians save $200+ by booking when the algorithm signals a low. Enter your nearest airport (Sydney, Melbourne, Brisbane), and search “anywhere” for your target month. Note the cheapest return fare.

- Daily budget: Hostel dorm in Southeast Asia? $30–50/day. Budget hotel in Europe? $80–120/day. Japan mid-range? $100–150/day.

- Multiply days, add flights, then add a 20% buffer. That buffer covers unexpected visa fees, travel insurance (compare options on Finder to find coverage that fits your budget), or that spontaneous cooking class.

Step 2 – Reverse-engineer your weekly target

Take your total trip cost and divide it by the number of weeks until your planned departure.

Pro tip: Use ASIC’s free MoneySmart budget planner to map your current spending before setting your weekly travel savings target—it takes 10 minutes and reveals hidden cash flow.

Example: A 2-week trip to Thailand costs $2,800 (flights $800 + $100/day × 14 days + buffer). You want to leave in 10 months (40 weeks). $2,800 ÷ 40 = $70 per week.

Does $70 a week feel doable? For someone earning $55,000 after tax (roughly $900 per week), that’s about 8% of your income. Tight but achievable.

Step 3 – Automate before you see the money

Pay yourself first: set up auto-transfers so your travel fund grows before you’re tempted to spend. Open a separate high-interest savings account – not linked to your everyday card. Set up an automatic transfer for payday (or the day after, to avoid overdrafts). Even $20 feels different when it happens without thinking.

Australian banks to consider:

| Bank | Key Benefit | Best For |

|---|---|---|

| ING Savings Maximiser | 5.5% p.a. (with conditions) | Consistent savers who can deposit $1k+/mo |

| UBank | No fees, auto-sweep feature | Set-and-forget automation |

| BOQ | Up to 5.4% p.a. for under 35s | Young professionals starting out |

For a full comparison of high-interest savings accounts, check Mozo’s latest rate table to see which bank matches your saving habits—rates change monthly, so verify before opening.

Step 4 – Attack one spending leak per fortnight

Don’t overhaul everything at once. You’ll burn out by week two. Instead:

- Fortnight 1: Reduce takeaway from four times to two times (save $40)

- Fortnight 2: Cancel two unused subscriptions (save $25)

- Fortnight 3: Switch from Woolies delivery to store pickup (save $10 delivery fee per shop)

Each change feels small. Stacked together, they build momentum.

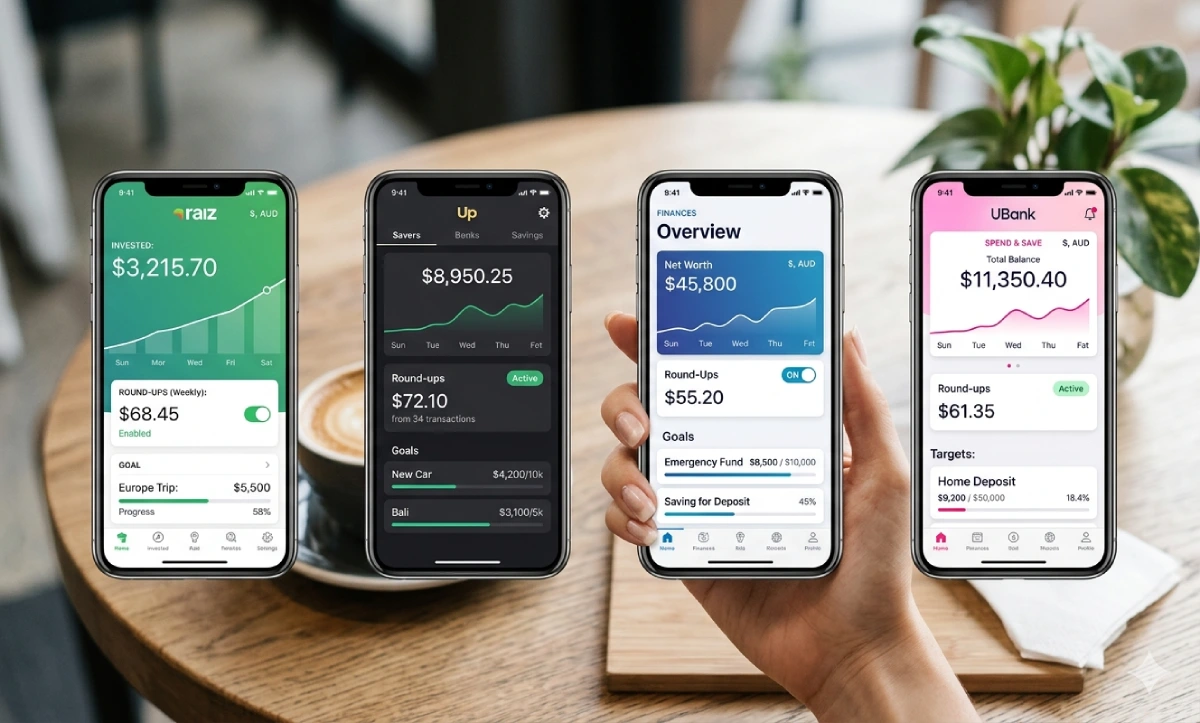

5 Micro-Saving Apps That Work in Australia (Set & Forget)

You don’t need willpower. You need invisible systems. These apps do the heavy lifting while you sleep.

Raiz

Round-ups from your everyday purchases (that $4.50 coffee becomes $5, with 50c invested). You can also set recurring deposits. The visual progress bar is weirdly addictive. Best for: hands-off micro-investing with round-ups.

Up Bank

Not strictly a savings app, but Up’s “Savers” feature lets you create separate buckets (e.g., “Japan Trip”) and auto-sweep a percentage of every payment into them. Plus, you can round up to the nearest $5 or $10.

Frollo

A free budgeting app that connects to over 120 Australian banks. It categorises your spending automatically and shows you exactly where your money goes. Sometimes visibility alone changes behaviour.

Goodments

Ethical round-up investing if you want your travel savings to grow while avoiding fossil fuels or gambling stocks. Best for: travellers with 18+ month timelines who prioritise values-aligned investing. Note: Both Raiz and Goodments involve market risk; use only for trips 18+ months away.

Squirrel (or similar micro-saver)

Apps like Twyp or Bamboo offer micro-saving features, but for pure simplicity: set up a second bank account (Up or UBank) with an automatic transfer of $5 daily. That’s $150 a month you’ll never miss.

Here’s the trick: when savings happen automatically, you adapt to living on what’s left – without the willpower drain. A $3 round-up feels like nothing. Fifty of them feel like $150. Your brain adapts to the new baseline within two weeks.

The ‘Invisible Money’ Strategy – Rewards, Cashback & Points (Without Extra Spending)

This isn’t about credit card churning or complicated spreadsheets. It’s about redirecting money you’re already spending.

Scan your card every single time. Even for a loaf of bread. Then:

- Convert Flybuys points to Coles gift cards ($10 = 2,000 points)

- Convert Everyday Rewards points to Woolies gift cards

- Here’s the trick: Use that “free” gift card for your normal grocery shop. Then take the cash you would have spent and transfer it directly to your travel fund.

One Coles shop a week at $80 – using a $10 gift card means you physically move $10 into savings. Over a year, that’s $520 without changing a single habit.

Cashrewards and ShopBack are the big players in Australia. Install the browser extension. When you shop online at Chemist Warehouse, Kmart, Booking.com, The Iconic, or even Officeworks, you get 2–15% cashback.

Example: Booking your future flights through Cashrewards might earn 3–5% back. That’s $30–50 on a $1,000 flight. Not life-changing, but it’s free money for something you were buying anyway.

Never buy something just for points or cashback. Only stack offers on planned spending. Set a reminder to check your cashback balance every two months and withdraw it to your travel account.

Realistic Side Hustles for Time-Poor Aussies (No Uber Eats Marathons)

You don’t need a second job. You need a side lever that pays $50–100 per week with minimal ongoing commitment.

Airtasker for micro-gigs

Post your skills: furniture assembly, dog washing, flyer drops, even standing in line for new sneaker releases. Target one job per weekend at $50–100. That’s $200–400 a month straight into your travel fund.

Market research & user testing

Octopus Group pays $30–60 per hour for focus groups and surveys. UserTesting pays $10–30 for 20-minute website feedback videos. Do one test before work or during lunch. That’s one hostel night in Bangkok earned.

Selling digital clutter

List clothes on Facebook Marketplace, textbooks on StudentVIP, and electronics on Gumtree. Students: sell last semester’s notes on Nexus Notes or Thinkswap. One textbook sale at $50 = your weekly travel target done.

The ‘one side hustle shift = one travel day’ rule

Reframe your effort: three hours of user testing ($60) = one night in a Bangkok hostel. One Airtasker furniture assembly ($80) = dinner and drinks in Bali. Suddenly, work doesn’t feel like work – it feels like trading time for experiences.

How Much Do You Really Need to Save for Your Dream Trip? (Real Australian Examples)

Let’s ditch the vague estimates. Here’s what real trips cost from Australia, with realistic weekly savings targets based on a take-home pay of ~$900/week (roughly $55k salary after tax).

The 3-step formula (featured snippet ready)

- Flights + insurance (use Skyscanner + compare travel insurance on Finder)

- Daily spend × number of days (hostels/budget accomm + local food + activities)

- Add 20% buffer for emergencies, splurges, or currency fluctuations

Example 1 – Bali on a budget (10 days)

- Return flights: $450 (Jetstar sale from Melbourne)

- Accom + food + scooter: $60/day × 10 = $600

- Travel insurance: $80

- Buffer (20%): $226

- Total: $1,356 – call it $1,500

Weekly save target: $1,500 ÷ 30 weeks = $50/week

Example 2 – Europe backpacking (4 weeks)

- Return flights: $1,600 (off-peak, one stop)

- Hostel dorms + Eurail + groceries: $110/day × 28 = $3,080

- Insurance + phone sim: $150

- Buffer: $966

- Total: $5,796 – call it $6,000

Weekly save target: $6,000 ÷ 52 weeks = $115/week (or $75/week + one side hustle shift)

Example 3 – Japan moderate budget (2 weeks)

- Return flights: $1,000 (sale fare via Cairns)

- Budget hotels + transit pass + food: $130/day × 14 = $1,820

- Insurance + pocket Wi-Fi: $120

- Buffer: $588

- Total: $3,528 – call it $3,500

Weekly save target: $3,500 ÷ 40 weeks = $87.50/week

How Sarah from Brisbane saved $3,000 in 6 months on a $55k salary?

Sarah worked as a receptionist (take-home ~$850/week after rent in a share house). She:

- Automated $40/week into a UBank saver

- Did one Airtasker dog-walk per weekend ($60)

- Used Flybuys points for groceries and moved the “saved” $20/week into her travel account

- Sold old clothes on Marketplace ($150 total)

Total saved in 6 months: $1,040 (auto) + $1,440 (side hustle) + $520 (Flybuys trick) + $150 (clothes) = $3,150. She flew to Vietnam for 3 weeks and came home with money left over.

The 3 Most Common Ways Australians Sabotage Their Travel Savings (And How to Fix Them)

#1 – The ‘mental account’ trap

You keep your travel money in your everyday account. Then you see a sale at Kmart and think, “I’ll just put it back next week.” Spoiler: you won’t.

Fix: Name a separate account something emotional like “Bali or Bust” or “Europe ’26”. Rename it in your banking app. When the money has a job, you’re less likely to steal from it. Note: While some travel sites offer Afterpay, remember: paying interest on a holiday undermines your savings goal. Use BNPL only if you can repay before the due date—and never for flights you can’t afford outright.

#2 – Social spending FOMO

Your friends want to have dinner and drinks every Friday. You’re trying to save. Saying “I can’t afford it” feels shameful, so you go and feel resentful.

Fix: Say, “I’m saving for a massive trip right now – can we do a picnic in the park instead? I’ll bring snacks.” Most friends will cheer you on. The ones who don’t? That’s a different problem.

#3 – Ignoring irregular expenses

Car rego ($800), dentist ($200), Christmas presents ($400). These always destroy your savings because you never planned for them.

Add a “life happens” buffer to your weekly target. If your trip needs $70/week, save $85/week. The extra $15 covers the surprises, so you never raid the travel fund.

Realistic Timelines Based on Your Income (Be Kind to Yourself)

Don’t compare your savings journey to someone else’s highlight reel. Your timeline works for your life – and that’s exactly how it should be.

If you can save $30/week

- Yearly total: $1,560

- Your trip: Domestic road trip (Great Ocean Road, Byron to Brisbane) or 1 week in New Zealand (South Island budget)

- Timeline: 10–12 months

If you can save $60/week

- Yearly total: $3,120

- Your trip: Bali/Thailand/Vietnam for 10–14 days

- Timeline: 10–12 months

If you can save $100/week

- Yearly total: $5,200

- Your trip: Europe or Japan for 3–4 weeks (budget style)

- Timeline: 12–14 months

It’s completely fine to take 18 months or even 2 years. The destination will still be there. What matters is that you arrive without credit card debt.

How to Stay Motivated When Saving Feels Slow (The Visual Trick That Works)

Motivation fades around week seven. Here’s how to push through.

Draw a large thermometer on butcher paper. Each $100 saved, colour in a segment. Stick it on your fridge. There’s something primal about watching that red line climb.

Celebrate micro-milestones:

- First $500 saved? Cook a meal from your destination (pad thai, tapas, ramen).

- Halfway there? Watch a travel documentary or buy one useful item (packing cubes, power bank).

- $100 to go? Invite a friend over and do a practice pack.

Share your weekly savings amount with someone who won’t judge. No shame, just honesty. Text them every Sunday night. “This week I saved $45. Next week’s target is $60.” You’d be surprised how much a little external witness helps.

FAQs

Is it realistic to save for a big trip on minimum wage in Australia?

Yes, but your timeline will stretch to 18–24 months, and you’ll need a side hustle. Minimum wage is roughly $45,000 before tax (~$720/week after tax). If you’re in a share house outside the CBD (e.g., Footscray, Morningside, Parramatta) and use Flybuys rigorously, saving $30–40/week is achievable. That’s $1,500–2,000 a year – enough for Bali or Fiji.

What’s the best bank account to save for travel in Australia?

For most people under 35: BOQ (up to 5.4% p.a. with no monthly fees). For consistent savers: ING (5.5% p.a., but you must deposit $1,000+ monthly and make 5 card transactions). For set-and-forget: UBank (automatic sweeps, no hoops to jump through). Pro tip: Use ASIC’s free MoneySmart budget planner to map your current spending before choosing an account.

How do I save for a trip when I still have HECS debt?

HECS is indexed to inflation (around 3–4% recently) but has no compounding interest. Voluntary repayments don’t reduce your compulsory repayments. Prioritise travel savings. The memory of a trip at 25 is worth more than clearing HECS early. Just ensure your compulsory repayments are covered by your employer’s withholding.

Can I use my superannuation to fund a big trip?

Rarely. Early release of super is only allowed for severe financial hardship (unable to pay rent or medical bills) or compassionate grounds (life-saving medical treatment). Using super for travel would incur massive tax penalties and rob your retirement. Don’t do it.

What’s the fastest way to save $3,000 on a tight income?

Combine three levers simultaneously:

- Automated saving: $40/week from your pay

- Side hustle: $30/week from Airtasker or user testing

- Cashback/rewards: $15/week from Flybuys gift card redirects

That’s $85/week × 35 weeks = $2,975. Or add a Marketplace sale ($100–200) to hit $3,000 in 33 weeks.

You Don’t Need More Money. You Need a Different System.

Here’s what I want you to walk away with: saving for a big trip on a tight income isn’t about deprivation or perfection. It’s about building tiny, automated systems that work with your Australian reality – rent, HECS, casual shifts, and all.

Start with one action this week. Not five. One.

Open that separate bank account. Or download Up. Or set up a $20 automatic transfer for your next payday. That’s it. Then next week, add the Flybuys trick. The week after, try one Airtasker gig.

Consistent small steps beat occasional big leaps. Keep going – your future self is already packing.

Your trip is waiting. Let’s go get it.

Have you started saving for a trip? What’s your destination – and which strategy are you trying first? Drop a comment below or tag us on Instagram. We’d love to cheer you on.