You should prioritize high-interest debt first because it grows faster than any other balance you owe. Credit cards often charge 20% or more in interest, so unpaid balances snowball quickly. Paying these off first saves money, shortens your payoff timeline, and frees up cash for other financial goals.

- What Counts as High-Interest Debt

- Why High-Interest Debt Grows So Fast

- The Debt Avalanche Method Explained

- Avalanche vs. Snowball: Which One Actually Saves You Money

- A Real Example of the Cost Difference

- How to Start Prioritizing Your Debt Today

- Common Mistakes That Slow You Down

- When Other Options Might Help

- The Bottom Line

Debt feels heavy when you’re juggling several payments at once. A credit card here, a personal loan there, maybe a car payment too. It’s easy to just pay whatever’s due each month and hope the balances shrink over time.

But not all debt is created equal. Some loans cost you far more than others, and if you don’t deal with them first, they can eat away at your progress no matter how much you pay. That’s why you need to prioritize high-interest debt first. It’s the single most effective move you can make to get out of debt faster and keep more of your own money.

What Counts as High-Interest Debt

High-interest debt usually means anything with an annual percentage rate, or APR, above 15%. Credit cards are the biggest culprit here. Right now, the average credit card APR in the U.S. sits somewhere between 20% and 23%, depending on your credit score and the card issuer. Some cards charge even more, especially for borrowers with fair or poor credit.

Payday loans and certain personal loans can carry similarly steep rates. Compare that to a mortgage, which might sit around 6% to 7%, or a federal student loan, often in the 5% to 8% range. The gap is huge. A dollar of credit card debt costs three or four times more than a dollar of mortgage debt, just sitting there.

This is why lumping all your debt together and paying it down evenly doesn’t make sense. The interest rate, not the balance size, tells you where your money is doing the most damage.

Why High-Interest Debt Grows So Fast

Interest compounds. That word gets thrown around a lot, but here’s what it actually means for you. Every month you carry a balance, the card issuer charges interest on what you owe, including any interest from the month before. Your debt doesn’t just sit still. It grows on itself.

Say you carry a $5,000 balance at 22% APR and only make minimum payments. Most of that minimum payment goes toward interest, not the actual amount you borrowed. It can take years to pay off, and you’ll likely spend well over $1,000 in interest along the way, sometimes much more depending on your payment size.

Now compare that to a lower-rate loan. The same $5,000 at 7% APR costs a fraction of that in interest over the same period. The math isn’t close. High-interest debt punishes you for every month you delay, which is exactly why it deserves your attention before anything else.

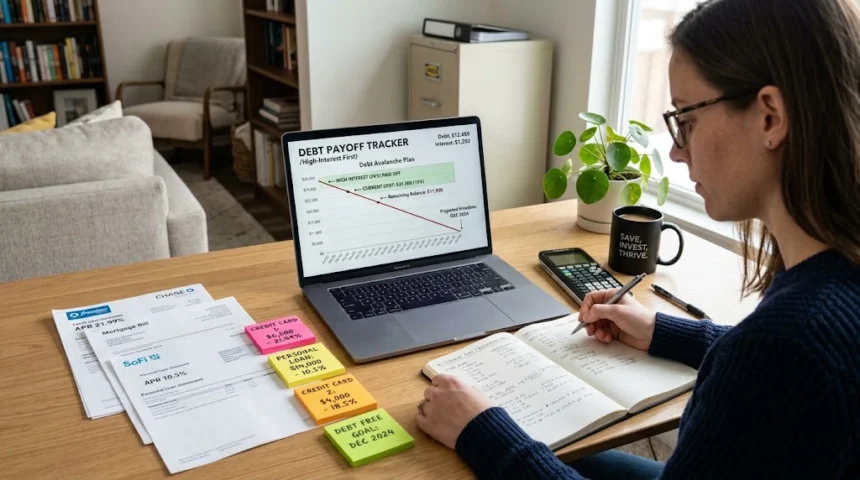

The Debt Avalanche Method Explained

Financial experts often recommend something called the debt avalanche method. The idea is simple. List every debt you have, from the highest interest rate to the lowest. Keep making minimum payments on everything. Then put any extra money you have toward the debt with the highest rate.

Once that one is paid off, roll the amount you were paying into the next highest-rate debt. Keep going until everything is cleared. This method targets the debt that’s costing you the most money first, which means you pay less interest overall and often get out of debt faster than you’d expect.

It requires a bit of discipline early on, especially if your highest-rate debt also happens to be your largest balance. But the payoff is real. You’re cutting off the fastest-growing part of your debt before it has more time to compound.

Avalanche vs. Snowball: Which One Actually Saves You Money

You may have heard of another popular strategy called the debt snowball method. Instead of ranking debts by interest rate, you rank them by balance size, smallest to largest. You pay off the smallest debt first, then move to the next smallest, and so on.

The snowball method has one real advantage. It gives you quick wins. Paying off a small balance fast feels good and can keep you motivated. For some people, that motivation matters more than the math.

But here’s the trade-off. If your smallest balance isn’t also your highest-rate debt, you’re letting that high-interest balance keep growing while you focus elsewhere. Over time, this usually costs you more money than the avalanche method. If saving the most money is your goal, prioritizing high-interest debt first almost always wins. If you know you need small victories to stay on track, a hybrid approach can work too, where you knock out one tiny balance for momentum, then switch to attacking the highest rate.

A Real Example of the Cost Difference

Let’s make this concrete. Imagine you have two debts: a credit card with a $3,000 balance at 22% APR, and a personal loan with a $3,000 balance at 8% APR. You have $200 extra each month to put toward debt beyond your minimum payments.

If you split that $200 evenly between both debts, you’ll pay them off slower and spend more in total interest. If you throw the entire $200 at the credit card first while paying only the minimum on the personal loan, you’ll clear the credit card months sooner. Once it’s gone, you redirect that same $200 plus your old credit card payment toward the personal loan, and it disappears fast too.

The total interest you pay across both debts drops significantly when you prioritize the higher rate first. Same income, same effort, less money wasted.

How to Start Prioritizing Your Debt Today

Start by listing every debt you owe. Write down the balance, the interest rate, and the minimum payment for each one. This single step gives you clarity most people never bother to get, and it makes the next decision obvious.

Rank your list from highest interest rate to lowest. Keep paying the minimum on everything except the top of the list. Put every extra dollar you can find toward that one debt. Look for small ways to free up cash too, like cutting a subscription or picking up a few extra hours of work, and send that money straight to your highest-rate balance.

Once your top debt is paid off, don’t celebrate by spending that freed-up money elsewhere. Roll it directly into the next debt on your list. This is what makes the avalanche method so powerful. Your payments get bigger over time, even though your total spending stays the same.

Common Mistakes That Slow You Down

One mistake people make is closing a paid-off credit card right away. This can actually hurt your credit score by reducing your available credit and shortening your credit history. Keep the card open, just don’t use it the same way.

Another mistake is ignoring interest rates entirely and paying off debts based on which one annoys you most emotionally. That’s understandable, but it costs money. If you truly need motivation, use the hybrid approach mentioned earlier rather than abandoning the strategy altogether.

Some people also stop tracking their progress. Debt payoff can take months or years, and it’s easy to lose momentum without a visual reminder of how far you’ve come. A simple spreadsheet or even a piece of paper on your fridge can keep you focused.

When Other Options Might Help

If your interest rates are extremely high, especially above 20%, it may be worth looking into a balance transfer card with a 0% introductory rate, or a debt consolidation loan with a lower fixed rate. These tools don’t replace the avalanche strategy. They work alongside it by lowering the rate you’re fighting against in the first place.

Just be careful with balance transfer fees, which typically run 3% to 5% of the amount transferred, and make sure you have a plan to pay off the balance before the introductory period ends. Otherwise, you could end up right back where you started, just with a new card.

The Bottom Line

Prioritizing high-interest debt first isn’t just a suggestion from finance blogs. It’s simple math. The longer a high-rate balance sits untouched, the more it costs you, and that cost compounds every single month. By ranking your debts by interest rate and attacking the worst one first, you keep more of your paycheck, shorten your payoff timeline, and build momentum that carries you all the way to debt-free.

You don’t need a big income or a financial degree to make this work. You just need a list, a plan, and the discipline to send extra money to the right place first.